Carta’s Q3 2025 Pre-Seed Report: “What It Means for Founders Right Now”

- Jason Engelhardt

- Jan 31

- 2 min read

Pre-seed isn’t dead. But it has changed.

Carta just published their Q3 2025 State of Pre-Seed, based on data from 10,000+ companies, and it explains why so many founders feel fundraising is harder and what to do about it.

What this report is (credibility + caveat). This is aggregated, anonymized Carta dataSAFEs and convertible notes covering Q1 2021 through Q3 2025, with a snapshot date of Nov 12, 2025. Not advice, but it’s a useful market thermometer.

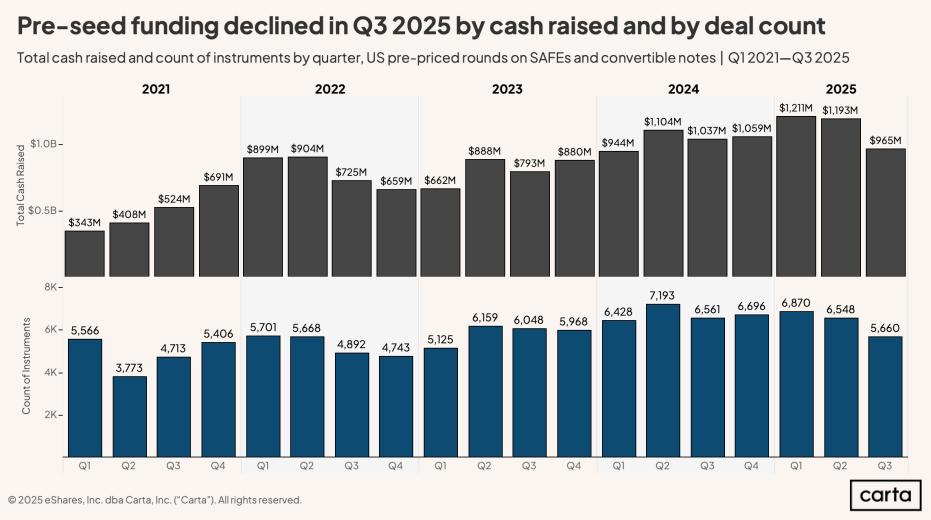

Trend #1 — Pre-seed cooled in Q3Q3

2025 declined in both total dollars and deal count. That doesn’t mean no one’s investing—it means investors are picking their spots, moving more slowly, and demanding clearer milestones.

.

Trend #2 — The rise of the ‘proof round.’

Here’s the big one: in Q3, about 45% of rounds were under $250K. That’s a signal that founders are raising smaller rounds to prove one or two things—before going for a larger pre-seed or seed round.

Trend #3 — Capital concentration

Across the first three quarters of 2025 vs 2024: more rounds under $1M, fewer above $1M—but total cash in the $1M+ bucket is actually higher. Translation: fewer big rounds, but when investors commit, the checks can be larger.

Trend #4 — SAFEs are the default + cap behavior

SAFEs dominate pre-seed, and post-money SAFEs are now the standard. Valuation caps are mostly stable, but for larger rounds—$2.5M+—caps have moved up. Bigger rounds = bigger expectations, and often bigger dilution risk if you’re not careful.

Trend #5 — Industry + geography snapshots

Healthtech stood out: $319M raised in 2025 YTD and high valuation caps—median $35M for large rounds. Also, the West still captures about half of U.S. pre-seed dollars, with the Bay Area leading, followed by New York, Boston, LA, and DC.

Founder playbook (actionable takeaways). So, what should founders do?

Raise to a milestone, not a number. Define the proof point your next investor needs.

If you’re raising small, make it intentional: timeline, milestones, and a crisp story.

Instrument choice matters—post-money SAFE is common, but understand dilution mechanics.

If you’re in sectors like biotech/energy, notes may still be more common—match investor expectations.

Don’t ignore geography—but don’t let it limit you. Build signal (traction, pilots, revenue, retention).

Here is the full Carta report on this page so you can download it. I’d love to hear what you’re seeing: smaller proof rounds or fewer, but bigger checks?

Comments